The Digital Panopticon: How Modern Investing Became a High-Stakes Game of Mirrors

The global financial theater of 2026 presents a paradox that would have been unimaginable a decade ago. We are told we live in the most empowered era for the individual saver, a time when Modern Investing has finally shed its elitist skin to become a tool of the masses. With a single biometric scan on a smartphone, anyone from a college student in Ambala to a retiree in New York can access global derivatives, fractional shares, and algorithmic portfolios. Yet, this “democratization” of Modern Investing is often a carefully constructed facade—a digital panopticon where every retail move is tracked, monetized, and countered by institutional giants.

To understand the current state of Modern Investing, one must first accept that the market is no longer a simple auction house for company ownership. It has transformed into a high-frequency, AI-driven liquidity machine. The very term Modern Investing has become synonymous with a specific type of digital frictionlessness that feels like freedom but often functions as a trap. When the barriers to entry fell, the complexity of the traps rose to meet them. We are no longer just investing in companies; we are investing in a complex technological stack where the “user experience” is often the product being sold, rather than the underlying financial performance.

The Illusion of Free in the Era of Modern Investing

The cornerstone of the Modern Investing narrative is the “zero-commission” trade. This was the Trojan Horse that allowed the industry to pivot from a transparent fee-for-service model to a predatory data-as-a-service model. In the world of Modern Investing, if you aren’t paying for the trade, you are the inventory. Through Payment for Order Flow (PFOF), your intent—your “buy” or “sell” signal—is auctioned off to high-frequency trading (HFT) firms before your order even hits the exchange. These firms use sub-millisecond advantages to skim the “spread,” a hidden tax that makes Modern Investing significantly more expensive than the “old-fashioned” way of paying a flat $5 fee.

This structural rot is rarely discussed by financial advisors because they, too, are navigating a shifting landscape. The traditional advisor has had to adapt to Modern Investing by becoming a hybrid of a therapist and a software reseller. They point to sophisticated-looking dashboards and “risk-tolerance sliders,” but these are often just window dressing for the same high-cost mutual funds and “closet index” strategies that have plagued the industry for years. The advisor’s role in Modern Investing has increasingly become about justifying a 1% management fee in an era where a “robo-advisor” can perform the same mechanical rebalancing for a tenth of the cost.

The Gamification Trap and Behavioral Exploitation

Perhaps the most insidious element of Modern Investing is its marriage to the attention economy. The platforms we use for Modern Investing are built by the same engineers who designed the most addictive social media apps. They utilize variable rewards, haptic feedback, and “social proof” to keep users engaged. In the context of Modern Investing, “engagement” is the enemy of “returns.” The more you check your app, the more likely you are to react to short-term volatility. The more you react, the more trades you execute. And every trade is a revenue event for the platform, even if it is a wealth-destruction event for you.

This gamification has led to the “Robinhood-ification” of the global markets, where “YOLO” trades and meme-stock frenzies are treated as legitimate strategies within the framework of Modern Investing. Advisors often play into this by offering “satellite portfolios”—small slices of your wealth they allow you to “play with” in the Modern Investing casino—just to keep you from interfering with the “core” portfolio they manage. It is a cynical acknowledgement that in the age of Modern Investing, the human brain is a liability to be managed, not an asset to be utilized.

The Passive Indexing Crisis

Furthermore, Modern Investing has reached a tipping point with the cult of the “Passive Index.” By funneling trillions of dollars into a handful of market-cap-weighted funds, Modern Investing has created a massive valuation distortion. When everyone buys the “index,” they are blindly buying the most expensive stocks, regardless of their fundamentals. This has stripped the market of its traditional role in price discovery. In the regime of Modern Investing, being a “disciplined indexer” actually means you are concentrating your wealth in a shrinking pool of mega-cap tech companies, creating a systemic risk that traditional diversification models are ill-equipped to handle.

Your advisor won’t warn you about the “Index Bubble” because the shift to passive vehicles has been their greatest labor-saving device. It is much easier to sell a “diversified portfolio” of three ETFs than it is to perform the rigorous security analysis that used to define the profession. Modern Investing has effectively automated the advisor’s job, but it hasn’t automated away their fee.

Why We Must Look Behind the Screen

As we navigate the rest of 2026, the stakes of understanding the mechanics of Modern Investing have never been higher. With inflation eroding the “real” value of static cash and the traditional safety of bonds appearing more like “returnless risk,” the pressure to participate in the equity markets is immense. But to enter the arena of Modern Investing without understanding the hidden taxes, the psychological nudges, and the structural imbalances is to invite slow financial decay.

The “Ugly Truths” that follow are the keys to reclaiming your agency in a system that wants you to remain a passive, predictable data point. We must peel back the neon lights of the Modern Investing apps and the polished brochures of the wealth managers to see the gears of extraction grinding underneath. To survive and thrive, you must learn to use the tools of Modern Investing without becoming a tool of the industry yourself.

10 Ugly Truths About Modern Investing

The sleek interface of your favorite investing app, the reassuring nod of a wealth manager, and the 24/7 ticker of financial news all point toward one comfortable narrative: Modern Investing has never been easier, safer, or more democratic.

But as we navigate 2026, the gap between “market marketing” and “market reality” has widened into a canyon. While financial advisors often present a polished strategy designed to keep you calm (and keep their fees coming), there are structural rot and psychological traps they rarely mention.

Behind the “commission-free” trades and “personalized” portfolios lie truths that could fundamentally alter your net worth. Here are the 10 ugly truths about modern investing that the industry isn’t telling you.

1. “Commission-Free” is the Most Expensive Way to Trade

The death of the $9.99 trade fee was hailed as a victory for the little guy. In reality, it was a pivot toward a more predatory model. Most modern platforms rely on Payment for Order Flow (PFOF). Instead of charging you, they sell your “buy” order to high-frequency trading firms. These firms execute your trade at a fraction of a cent higher than the best price, skimming off the top before you even own the stock.

Over a lifetime of “free” trades, this microscopic price slippage can cost you thousands in lost gains. Your advisor won’t tell you this because their own firm often benefits from similar back-end liquidity arrangements.

2. The “Passive” Index Bubble is Warping Reality

We’ve been told that index funds are the ultimate “set it and forget it” tool. However, in 2026, the sheer volume of money flowing into passive vehicles has created a price discovery crisis. When everyone buys the “index,” money flows into the biggest companies regardless of their actual health or valuation.

This creates a self-fulfilling prophecy where the “Big 7” or “Big 10” stocks become too big to fail—until they aren’t. If the passive bubble pops, the lack of active buyers to catch the falling knives means the crash will be faster and deeper than anything we saw in 2008 or 2020.

3. Your Advisor is a “Salesperson,” Not a “Sage”

Unless you are working with a strictly Fee-Only Fiduciary, your advisor likely has a “Fee-Based” model. This is a clever play on words. “Fee-Based” means they can charge you a flat fee and collect commissions from the products they sell you.

They might steer you toward a specific mutual fund not because it’s the best, but because it pays them a “kickback” (often called a 12b-1 fee). They hide this under the guise of “proprietary research” or “vetted selections.”

4. Modern Apps are Designed Like Casinos

The “Gamification” of investing is perhaps the most insidious development in Modern Investing. Features like:

- Confetti animations on completed trades.

- Leaderboards comparing your returns to others.

- Push notifications about “trending” stocks.

These aren’t “user-friendly” features; they are neurological triggers. They are designed to keep you trading frequently, because the more you trade, the more data the platform sells, and the more mistakes you make.

5. AI is Not Your Edge—It’s Your Competition

Advisors love to talk about how they use “AI-driven insights” to manage your money. The ugly truth? By the time a retail-facing AI identifies a “trend,” institutional grade Agentic AI Systems have already executed millions of trades and sucked the profit out of that opportunity. In the 2026 market, you aren’t using AI to win; you are competing against machines that can read a 10-K report and execute a trade in the time it takes you to blink.

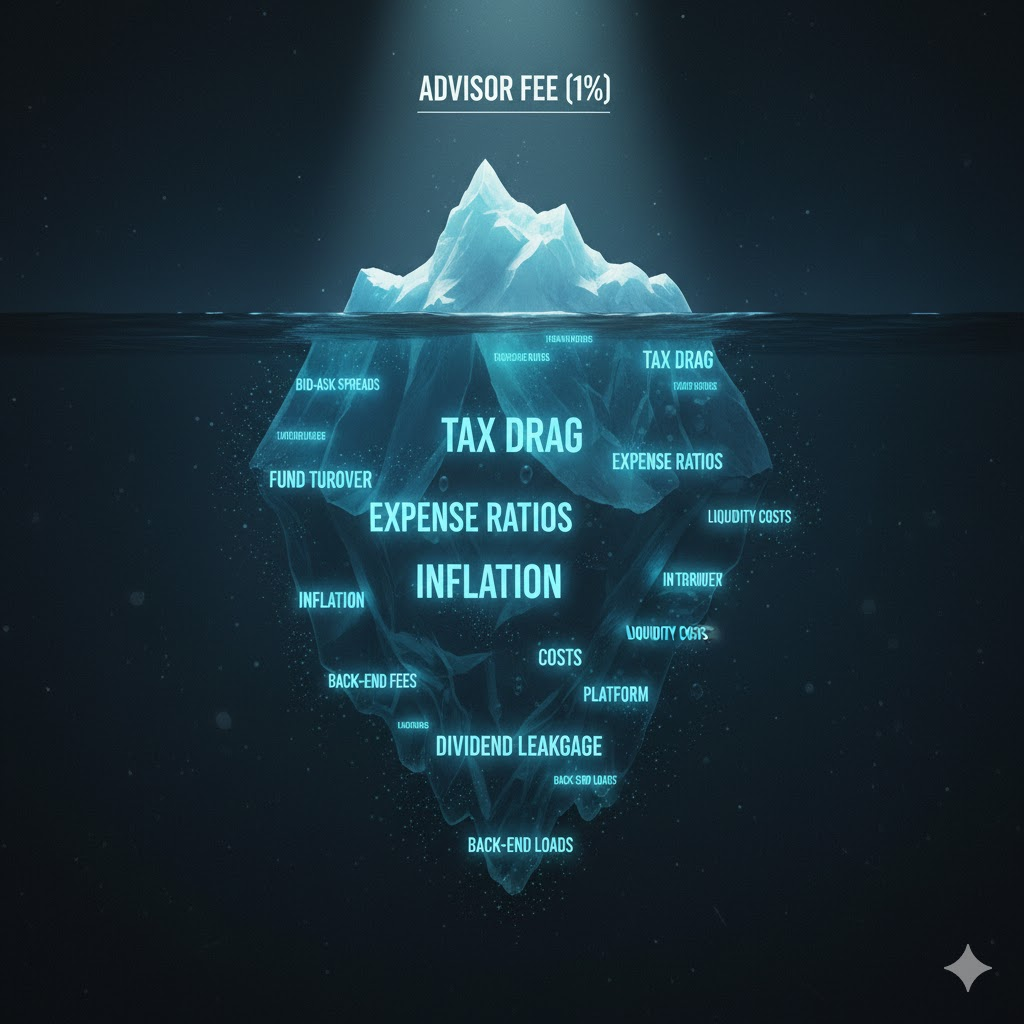

6. The “Tax Drag” is a Silent Killer

Advisors focus on “Gross Returns” because they look impressive on a brochure. They rarely talk about Tax Drag—the percentage of your returns lost to capital gains taxes, dividend taxes, and inefficient fund turnovers.

The Math: If your portfolio grows by 8%, but you lose 2% to taxes and 1.5% to advisor fees, your “real” growth is only 4.5%. Over 30 years, that “small” difference can mean the difference between retiring at 55 or 70.

7. Diversification is Often “Di-worse-ification”

Your advisor might have you spread across 15 different funds. They call it “risk management.” Often, it’s just a way to ensure they have a reason to charge a management fee. If you own four different “Large Cap” funds, you likely own the same 50 stocks four times over. This doesn’t protect you; it just guarantees you will never beat the market, while you pay multiple layers of expense ratios.

8. Inflation is Much Higher for Investors

The Consumer Price Index (CPI) measures the cost of milk and eggs. But for an investor, the “Inflation” that matters is the Asset Inflation—the rising cost of buying a house, a share of a top-tier company, or a medical plan. While the government might claim 3% inflation, the cost of the things you actually want to buy with your wealth is often rising at 7-10%. Your advisor’s “conservative 5% return” plan might actually be losing you purchasing power every year.

9. ESG is Mostly a Marketing Gimmick

Environmental, Social, and Governance (ESG) investing is the darling of the 2020s. However, many ESG funds are just standard tech funds with a higher fee. They “greenwash” their holdings, including companies that have little to do with the environment but high scores on arbitrary checklists. You’re paying a premium for a “conscience” that is often just a rebranded S&P 500 fund.

10. The Best Advice is “Boring” (and Advisors Can’t Charge for Boring)

The secret to wealth in Modern Investing hasn’t changed in 100 years: spend less than you earn, invest in low-cost broad assets, and wait. But an advisor can’t charge you 1.5% a year to tell you to “do nothing.” To justify their existence, they must create complexity—rebalancing, tactical shifts, and “alternative” assets. This activity often creates more costs than value.

How to Protect Yourself in 2026

To survive the era of Modern Investing, you must stop being a passive consumer of financial products and start being a skeptical architect of your own wealth.

| Feature | The Advisor’s Version | The Ugly Reality |

| Fees | “We only charge 1%.” | Real cost is often 3%+ when including fund fees and tax drag. |

| Volatility | “Market fluctuations are normal.” | High-speed Algos make crashes faster and more violent. |

| Strategy | “Active management beats the market.” | 90% of active managers fail to beat the index over 10 years. |

10 Ugly Truths About Modern Investing That Financial Advisors Hide

The sleek interface of your favorite investing app, the reassuring nod of a wealth manager, and the 24/7 ticker of financial news all point toward one comfortable narrative: Modern Investing has never been easier, safer, or more democratic.

But as we navigate 2026, the gap between “market marketing” and “market reality” has widened into a canyon. While financial advisors often present a polished strategy designed to keep you calm (and keep their fees coming), there are structural rot and psychological traps they rarely mention.

Behind the “commission-free” trades and “personalized” portfolios lie truths that could fundamentally alter your net worth. Here are the 10 ugly truths about modern investing that the industry isn’t telling you.

1. “Commission-Free” is the Most Expensive Way to Trade

The death of the $9.99 trade fee was hailed as a victory for the little guy. In reality, it was a pivot toward a more predatory model. Most modern platforms rely on Payment for Order Flow (PFOF). Instead of charging you, they sell your “buy” order to high-frequency trading firms. These firms execute your trade at a fraction of a cent higher than the best price, skimming off the top before you even own the stock.

Over a lifetime of “free” trades, this microscopic price slippage can cost you thousands in lost gains. Your advisor won’t tell you this because their own firm often benefits from similar back-end liquidity arrangements.

2. The “Passive” Index Bubble is Warping Reality

We’ve been told that index funds are the ultimate “set it and forget it” tool. However, in 2026, the sheer volume of money flowing into passive vehicles has created a price discovery crisis. When everyone buys the “index,” money flows into the biggest companies regardless of their actual health or valuation.

This creates a self-fulfilling prophecy where the “Big 7” or “Big 10” stocks become too big to fail—until they aren’t. If the passive bubble pops, the lack of active buyers to catch the falling knives means the crash will be faster and deeper than anything we saw in 2008 or 2020.

3. Your Advisor is a “Salesperson,” Not a “Sage”

Unless you are working with a strictly Fee-Only Fiduciary, your advisor likely has a “Fee-Based” model. This is a clever play on words. “Fee-Based” means they can charge you a flat fee and collect commissions from the products they sell you.

They might steer you toward a specific mutual fund not because it’s the best, but because it pays them a “kickback” (often called a 12b-1 fee). They hide this under the guise of “proprietary research” or “vetted selections.”

4. Modern Apps are Designed Like Casinos

The “Gamification” of investing is perhaps the most insidious development in Modern Investing. Features like:

- Confetti animations on completed trades.

- Leaderboards comparing your returns to others.

- Push notifications about “trending” stocks.

These aren’t “user-friendly” features; they are neurological triggers. They are designed to keep you trading frequently, because the more you trade, the more data the platform sells, and the more mistakes you make.

5. AI is Not Your Edge—It’s Your Competition

Advisors love to talk about how they use “AI-driven insights” to manage your money. The ugly truth? By the time a retail-facing AI identifies a “trend,” institutional grade Agentic AI Systems have already executed millions of trades and sucked the profit out of that opportunity. In the 2026 market, you aren’t using AI to win; you are competing against machines that can read a 10-K report and execute a trade in the time it takes you to blink.

6. The “Tax Drag” is a Silent Killer

Advisors focus on “Gross Returns” because they look impressive on a brochure. They rarely talk about Tax Drag—the percentage of your returns lost to capital gains taxes, dividend taxes, and inefficient fund turnovers.

The Math: If your portfolio grows by 8%, but you lose 2% to taxes and 1.5% to advisor fees, your “real” growth is only 4.5%. Over 30 years, that “small” difference can mean the difference between retiring at 55 or 70.

7. Diversification is Often “Di-worse-ification”

Your advisor might have you spread across 15 different funds. They call it “risk management.” Often, it’s just a way to ensure they have a reason to charge a management fee. If you own four different “Large Cap” funds, you likely own the same 50 stocks four times over. This doesn’t protect you; it just guarantees you will never beat the market, while you pay multiple layers of expense ratios.

8. Inflation is Much Higher for Investors

The Consumer Price Index (CPI) measures the cost of milk and eggs. But for an investor, the “Inflation” that matters is the Asset Inflation—the rising cost of buying a house, a share of a top-tier company, or a medical plan. While the government might claim 3% inflation, the cost of the things you actually want to buy with your wealth is often rising at 7-10%. Your advisor’s “conservative 5% return” plan might actually be losing you purchasing power every year.

9. ESG is Mostly a Marketing Gimmick

Environmental, Social, and Governance (ESG) investing is the darling of the 2020s. However, many ESG funds are just standard tech funds with a higher fee. They “greenwash” their holdings, including companies that have little to do with the environment but high scores on arbitrary checklists. You’re paying a premium for a “conscience” that is often just a rebranded S&P 500 fund.

10. The Best Advice is “Boring” (and Advisors Can’t Charge for Boring)

The secret to wealth in Modern Investing hasn’t changed in 100 years: spend less than you earn, invest in low-cost broad assets, and wait. But an advisor can’t charge you 1.5% a year to tell you to “do nothing.” To justify their existence, they must create complexity—rebalancing, tactical shifts, and “alternative” assets. This activity often creates more costs than value.

How to Protect Yourself in 2026

To survive the era of Modern Investing, you must stop being a passive consumer of financial products and start being a skeptical architect of your own wealth.

| Feature | The Advisor’s Version | The Ugly Reality |

| Fees | “We only charge 1%.” | Real cost is often 3%+ when including fund fees and tax drag. |

| Volatility | “Market fluctuations are normal.” | High-speed Algos make crashes faster and more violent. |

| Strategy | “Active management beats the market.” | 90% of active managers fail to beat the index over 10 years. |

Conclusion: Surviving the Mirage of Modern Investing

As we stand at the intersection of technological convenience and financial complexity, it is clear that Modern Investing is a double-edged sword. We have been sold a version of Modern Investing that promises total autonomy and effortless wealth, yet the reality is a system that thrives on investor noise, frequent turnover, and hidden structural leaks. The “ugly truths” we’ve uncovered aren’t meant to scare you away from the markets, but rather to shift your perspective from a passive consumer to a tactical participant in the Modern Investing ecosystem.

To truly master Modern Investing, one must recognize that the sleekest apps are often the ones designed to drain your capital through behavioral manipulation and microscopic price slippage. The financial advisors who claim to offer “cutting-edge” strategies are frequently just repackaging the same bloated, fee-heavy products that have existed for decades, now polished with the jargon of Modern Investing. In 2026, your greatest asset isn’t a premium subscription to a stock picker or an AI-driven bot; it is your ability to stay disciplined while the rest of the world is swept up in the gamified frenzy of Modern Investing.

The future of your wealth depends on your willingness to look beneath the surface. While Modern Investing offers more tools than ever before, it also demands a higher level of skepticism. You must be the one to audit your “tax drag,” to question the “passive” nature of your index funds, and to demand absolute fiduciary transparency. If you can filter out the high-frequency distractions and focus on low-cost, long-term value, you can turn the predatory mechanics of Modern Investing into a vehicle for genuine financial freedom.

In the end, Modern Investing shouldn’t be about chasing the next digital gold rush or reacting to every notification on your phone. It should be a quiet, calculated process of building a resilient future. The industry will continue to evolve, finding new ways to monetize your attention and your trades, but by staying informed of these hidden truths, you ensure that the primary beneficiary of Modern Investing is you—not your broker, not your advisor, and certainly not the algorithms.